It’s July, which means it’s about time to do a mid-year check-in (WHERE DID HALF THE YEAR GO?!). Personally as I do my check-in, I’m keeping in mind that a lot has changed since January. Between political uncertainties and battling the pandemic, my 2020 goals look like they were written in an alternate timeline and require significant adjustments, if not overhauling, and that’s ok. The goals still did their job as a directional force, which was especially helpful in incredible times of uncertainty.

Now if you need some help readjusting your goals, here are 4 timeless tips I picked up from my conversation with Suraya Zainudin (Ringgit Oh Ringgit) and Aaron Tang (Mr. Stingy) at the start of the year about goals.

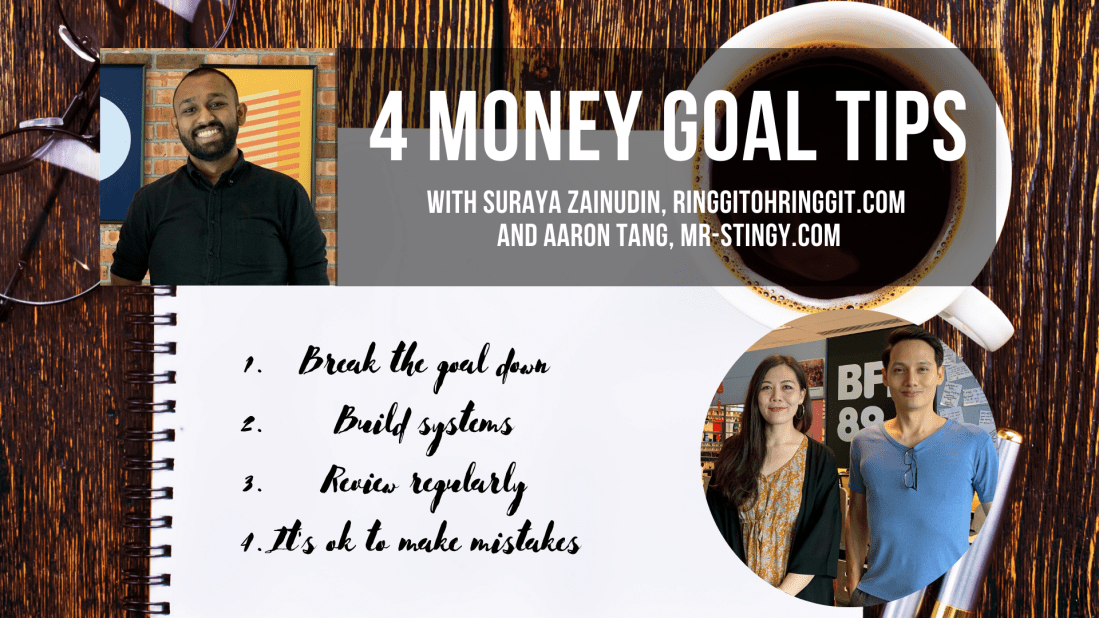

- Break the goal down instead of having one big ambiguous goal like ‘save more money’. Try something like ‘I will save 10% of my income every month’. That will clarify the goal, and with that help you achieve it.

- Build systems to help you achieve your goals. An example here related to the above-stated goal would be to automate your 10% savings, which is a feature available on most banking platforms. Set it up so that every month 10% of your income goes into another account so that you can’t “accidentally” use it up.

- Pro Tip: Personally I’ve set it up so that the money leaves my account a few days after my salary comes in, to be specific the 1st of the month. This way I start the month knowing that I’ve put money towards my different goals and commitments.

- Pro Pro Tip: Consider increasing your EPF contribution – that way you’ll tap into the power of compounding interest and you won’t be able to touch the money till you’re 55.

- Super Pro Tip: Think about trying a digital investment platform, like Stashaway. This will also tap into the power of compounding interest but with more flexibility.

- Review your goals. Take Mr. Stingy for example, he sets aside (a SMART goal approved) half a day every month to do a money review and keep aware of his finances. Don’t try and be a hero and say you’ll do it everyday, be realistic. I feel that it’s better to start small and grow, than to start big and stop soon.

- Mistakes will happen. You’re not perfect, remember that it’s ok to make mistakes or even fail, as long as your making progress and taking the right steps. Example: Suraya had some pretty moonshot goals, (like earning RM100,000 in 6 months!), and although she knows she might not achieve them the process of trying to get them done will move her forward!

I hope that these were helpful and I’d love to hear your own thoughts, tips, and strategies for goal setting! Let me know in the comments section below or hit me up on Twitter!

Now if you’ve got 20 minutes and want to hear more from Suraya and Aaron, check out the full episode on BFM, Spotify, Apple Podcasts or whenever you listen to podcasts. The episode is titled: Money Goal Tips With Mr. Stingy And ‘Ringgit Oh Ringgit’